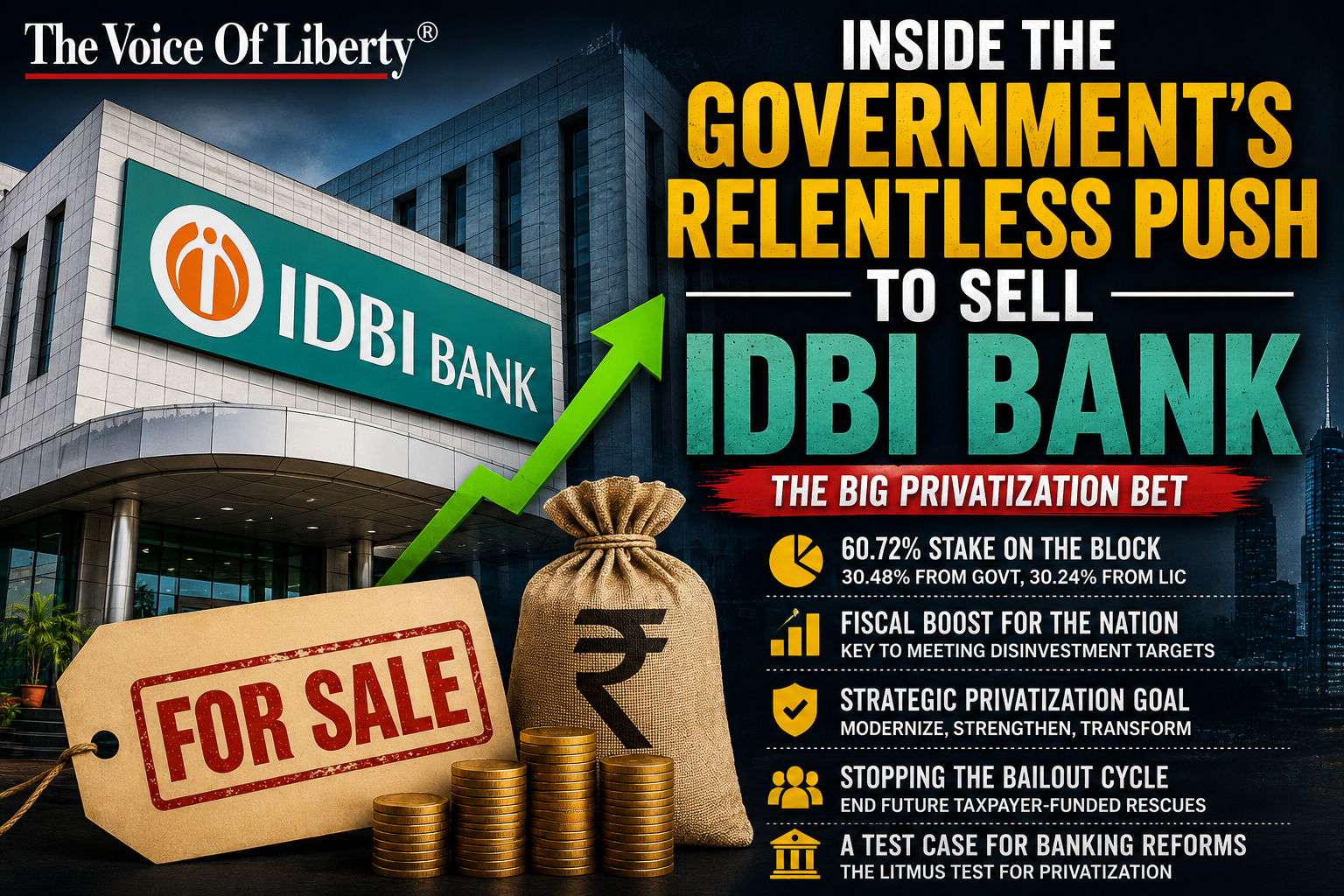

The Indian government is making one of its strongest pushes yet to privatize IDBI Bank, viewing the transaction as a landmark reform that could reshape the future of India’s banking sector.

The Centre, along with Life Insurance Corporation of India (LIC), plans to jointly sell a 60.72% stake in the lender while transferring management control to a strategic buyer. The government currently holds 30.48% of the bank, while LIC owns 30.24%.

The sale is widely seen as a test case for India’s broader privatization ambitions.

Why IDBI Bank Is Different

Among India’s state-backed lenders, IDBI Bank occupies a unique position.

Unlike most Public Sector Banks (PSBs), which are governed by special banking legislation, IDBI Bank operates under the Companies Act framework. This distinction significantly simplifies the privatization process.

For most government-owned banks, reducing state ownership below 51% would require legislative amendments approved by Parliament. In IDBI Bank’s case, management control can be transferred through corporate approvals without major legal restructuring.

This makes IDBI the most practical and legally viable candidate for India’s first major banking privatization.

A Key Piece of the Disinvestment Agenda

The proposed sale also plays a crucial role in the government’s fiscal planning.

Successive governments have relied on strategic disinvestment to generate non-tax revenue and fund infrastructure, welfare programs, and development initiatives. A successful IDBI transaction would unlock substantial capital and help advance broader asset monetization goals.

Economic policymakers view the deal as an important signal to both domestic and international investors regarding India’s commitment to structural reforms.

Why LIC Wants to Exit

LIC’s involvement in IDBI Bank originated from a rescue operation rather than a long-term investment strategy.

In 2018, LIC acquired a controlling stake in the bank when IDBI was struggling with high levels of bad loans and financial stress. The move was designed to stabilize the institution and restore confidence.

However, insurance regulators have long maintained that insurance companies should not indefinitely control commercial banks. As a result, LIC’s eventual exit has been expected for several years, aligning naturally with the government’s privatization plans.

A Bank That Has Recovered

The timing of the sale is not accidental.

A few years ago, IDBI Bank was burdened by mounting non-performing assets (NPAs) and was operating under the Reserve Bank of India’s Prompt Corrective Action (PCA) framework, which restricts lending and expansion activities for weak banks.

Since then, the lender has undergone a significant turnaround. Improved asset quality, stronger profitability, fresh capital infusions, and tighter risk management have helped restore its financial health.

Government officials believe the bank is now attractive enough to draw interest from major domestic and international investors.

Ending the Bailout Cycle

One of the broader arguments for privatization centers on reducing the burden on taxpayers.

Historically, public sector banks have periodically required government capital injections to maintain regulatory capital requirements. Supporters of privatization argue that private ownership can bring operational efficiency, technological modernization, stronger accountability, and access to fresh capital without relying on public funds.

The IDBI transaction is therefore viewed as an opportunity to permanently shift future capital requirements away from taxpayers.

The Roadblock

Despite strong government support, the sale process has faced challenges.

Reports indicate that financial bids received from interested investors fell below the government’s valuation expectations. Market volatility, global economic uncertainty, and geopolitical risks have weighed on investor appetite and pricing assumptions.

Rather than abandoning the effort, authorities are reportedly reviewing valuation frameworks and transaction structures to revive the process.

Why the Sale Matters

For the government, IDBI Bank is more than just another asset sale.

A successful privatization would demonstrate that banking-sector reforms can move beyond policy discussions into execution. It would also establish a blueprint for future privatization efforts and signal India’s willingness to reduce direct state ownership in commercial banking.

The outcome of the IDBI Bank sale may therefore determine not only the future of one lender, but also the credibility of India’s long-term banking reform agenda.